Hong Kong Enacted Legislation for a Two-tiered Profits Tax Rates Regime

Hong Kong Enacted Legislation for a Two-tiered Profits Tax Rates Regime

May 18, 2018

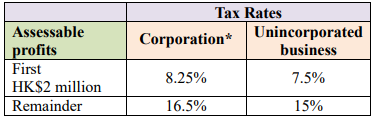

Inland Revenue (Amendment) (No.3) Ordinance 2018 for presenting a two-layered benefit assess rates administration was authorized on 29 March 2018. The two-tiered profits tax rates regime will be effective from the time of evaluation 2018/2019 (i.e. on or after 1 April 2018):

• In the event that a corporation is a partner of a partnership, the concessionary tax rate of 8.25% will just apply to the first HK$2 million pro-rated by its share in the partnership.

Prohibitive Provisions

The primary target of the regime is to decrease the taxation burden of SMEs and start-up organizations. To avoid group splitting income amongst various entities in order to appreciate the lower tax rate, restrictive provisions are presented which confine the utilization of the two-tiered tax rates to just a single entity nominated by a group of “connected” entities. The definition of “connected” entities can be found in our Hong Kong Tax News – January 2018.

No Double Benefits

Certain entities may have just enjoyed half tax rate under the current tax regimes, for example, reinsurance business, captive insurance business, corporate, treasury center, aircraft leasing business and aircraft leasing management business. In order to evade double benefits for taxpayers conveying these organizations, which have effectively elected to appreciate half tax rate, these taxpayers will be excepted from the two-tiered profits tax rates regime under the new law.

Income from QDIs not counted towards the First HK$2 million Threshold

The new law likewise stipulated that profits gotten from qualifying debt instruments (“QDIs”) which have been taxed at half tax rate under Section 14A of the Inland Income Ordinance (“IRO”) won’t be tallied towards the principal HK$2 million threshold under the two-tiered profits tax rates regime.

Provisional Profits Tax for Transitional Arrangement

Amid the transitional period, if the 2018/2019 provisional profits tax is imposed in view of the full tax rate for specific entities, the new law gives an extra ground to holdover of the 2018/2019 provisional profits tax where the entity is probably going to be chargeable under the two-tiered profits tax regime. The holdover application must be made in composing to the Commissioner inside the set time limit.

If you wish to explore on how to benefit from the two-tiered tax rates regime in Hong Kong, please contact our Hong Kong team at + 852 2654 8800 or email us at info@opkofinance.com