Withholding Corporate Income Tax in China

Withholding Corporate Income Tax in China

May 15, 2018

In China, withholding Corporate Income Tax (CIT) is applied to the following China-sourced incomes derived by non-resident enterprises without establishments in China, or to that derived by non-resident enterprises with establishments in China yet whose wage isn’t identified with these establishments:

• Interests, rents, and royalties and wage from the transfer of property; and

• Some other incomes subject to CIT obtained by non-resident enterprises.

The withholding CIT rate for non-tax resident enterprises in China is 20 percent (currently reduced to 10 percent). For dividends, interests, rents, and royalty income, if the particular rate in a tax treaty is higher than 10 percent, the 10 percent rate will win; if the tax treaty is lower than 10 percent, then the rate in the tax treaty should be adopted.

For instance, Hong Kong’s double tax agreement with China diminishes the withholding tax rate on dividends from 10 percent to five percent. This implies China-sourced dividends remitted to Hong Kong are liable to a reduced withholding rate of five percent.

The tax payable on income obtained by non-resident enterprises should to be withheld at the source, with the payer (i.e., the Chinese enterprise who remits the fund overseas) as the withholding agent.

The formula for calculating withholding tax liability is: Tax payable = Taxable income x Tax rate

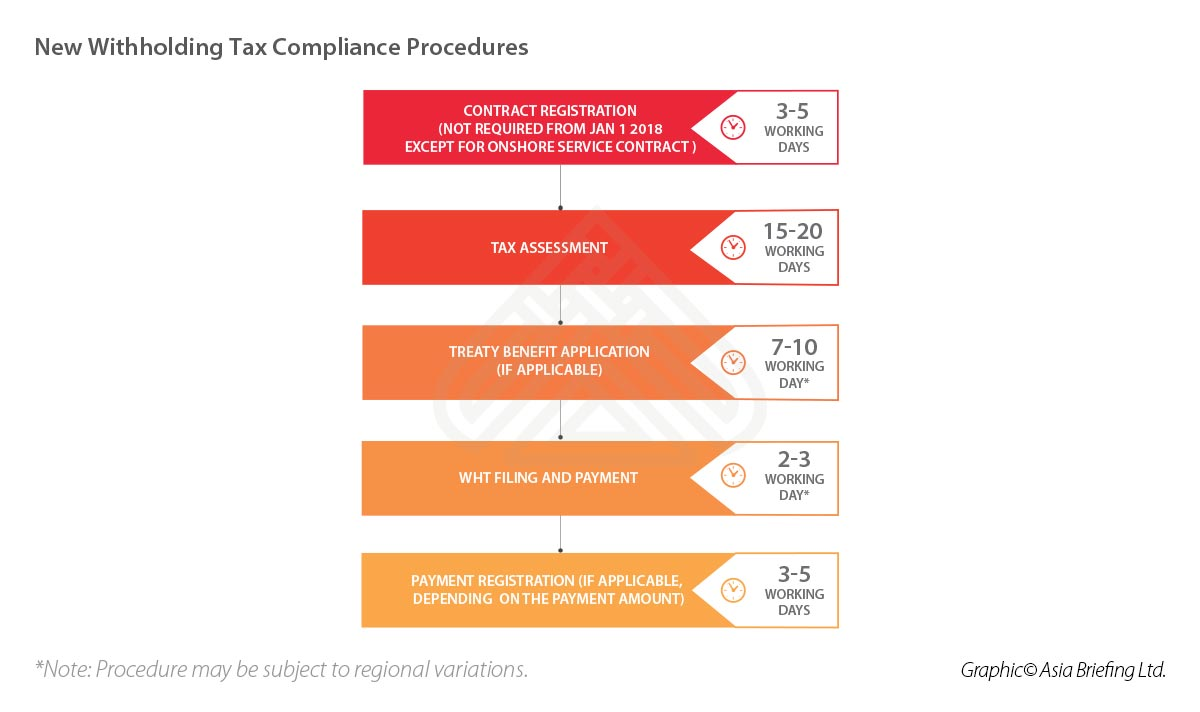

Filing process for withholding CIT

Where a non-resident enterprise obtains China-sourced dividends, interest, rents, and royalties, or income from property transfers, it is required to file the withholding tax either by itself or by a withholding agent.

With the SAT’s Announcement on Issues Relating to Withholding Tax on China-Sourced Income of Non-occupant Enterprises (SAT Announcement [2017] No.37, hereinafter Circular 37) coming into force on December 1, 2017, the filing procedure for withholding CIT was altogether cleared up and revised.

As indicated by Circular 37:

• The record-filing of the contract is no longer required.

Beforehand, a duplicate of the contract giving rise to the taxable income, alongside a contract registration record form and other applicable documents, must be submitted to the authorized tax bureau for record-fling within 30 days of signing the agreement. All documentation, incorporating those originally in a foreign language, must be converted into Chinese. This process enforced to each resulting revision, supplement, or extension of the contract.

Circular 37 diminished the burden on the withholding agent for record- filing, except in limited situations issued in other particular regulations, for example, SAT and SAFE Announcement [2013] No.40. The competent tax authorities still have the privilege to ask for the contract from the agent.

• The additional reporting requirement for income paid by installment is canceled.

Formerly, for income paid by installment, the withholding agent should, inside 15 days prior to making the last payment, report to the authorized tax bureau the details of all completed payments in order to complete a tax withholding clearance.

Circular 37 canceled this reporting requirement.

• The arising time of withholding obligation is revised.

Beforehand, the arising time of withholding obligations on equity investment income, such as dividends bonuses, should be the day on which the distribution decision was made by the board of directors or the actual payment date, whichever is prior.

Circular 37 cleared up that the time of withholding obligation emerging equity investment income should be the actual payment date.

Further, Circular 37 included that, where income of asset transfer is paid by installments, the installments would first be able to be dealt with as recovery of costs of previous investments, and the withholding CIT can be calculated and withheld upon recovery of all costs, i.e. upon receiving the last installment.

• The due date of the payment of withholding tax is relaxed.

Beforehand, the withholding agent needed to file and pay withholding commitments to tax authorities inside seven days of withholding obligations emerging. Furthermore, where the withholding agent neglected to withhold tax or was not able do as such, non- resident enterprises should file and pay withholding tax to the tax authorities, where the income was derived inside seven days from the date the payment is made by the withholding agent or from the date the payment winds up payable. If non- resident enterprises neglected to pay too, late payment interest would be forced.

Circular 37 gave a more valuable new rule. Where the non- resident enterprise has documented and paid tax before the tax authorities order it to make payment within a stipulated period, the enterprise might be esteemed to have paid tax on time. For this situation, late payment interest will not be levied.

What’s more, Circular 37 accommodates more prominent cooperation among various tax bureaus to enhance the business environment. For instance, when the non- resident enterprise creates income from various tax areas, the withholding agent can pay tax to only one of the significant tax bureaus.

Also, Circular 37 clarifies different issues relating with the estimation of taxable income, for example, the foreign exchange rule in calculation, the retrospective effect of specific standards, and how to calculate taxable income in equity transfer and asset transfer.

Please contact our Chinese team for any information regarding the tax laws and practice in China, at + 86 187 177 31958 or email us at info@opkofinance.com